Borrowing On Folks Finance

Q69. Let’s look at borrows on Folks.Finance a borrowing and lending protocol built on Algorand. We want to get an understanding of how what assets users most want to borrow, how often borrows are happening, and the average collateral ratio between the collateral offered and the asset that is borrows. Ultimately, we want to get a better understanding of what people are borrowing, and what the collateral ration looks like.

Introduction

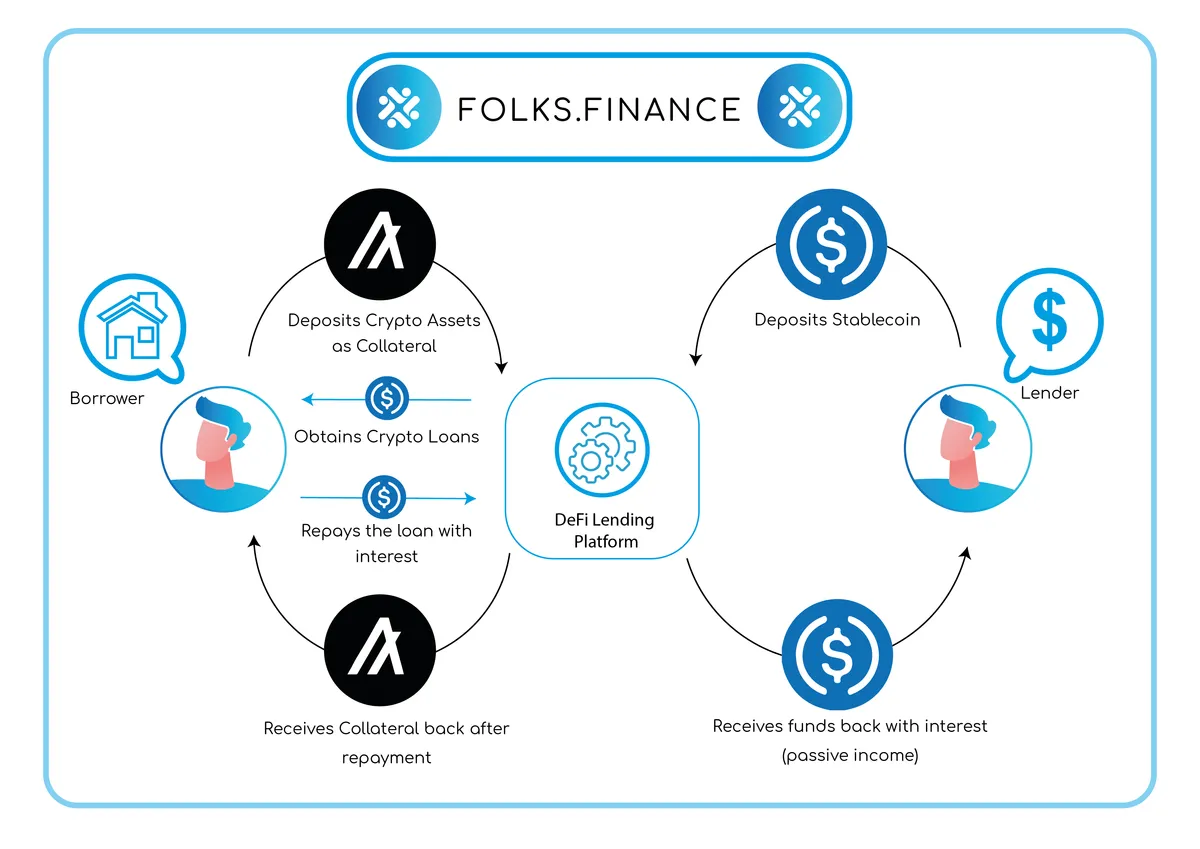

Folks Finance is a protocol offering decentralised services of borrowing and lending in a permissionless way over Algorand.There are two main actors in the platform:

-

Lenders who deposit their token for a passive income which comes from the borrowing interest. Lending asset are kept on a pool similarly to a liquidity pool on a swap and the rewards are paid taking into account the % of the pool each lenders holds.

-

Borrowers who get crypto loans backed by a deposited collateral. The loan amounts are transferred from the pool.

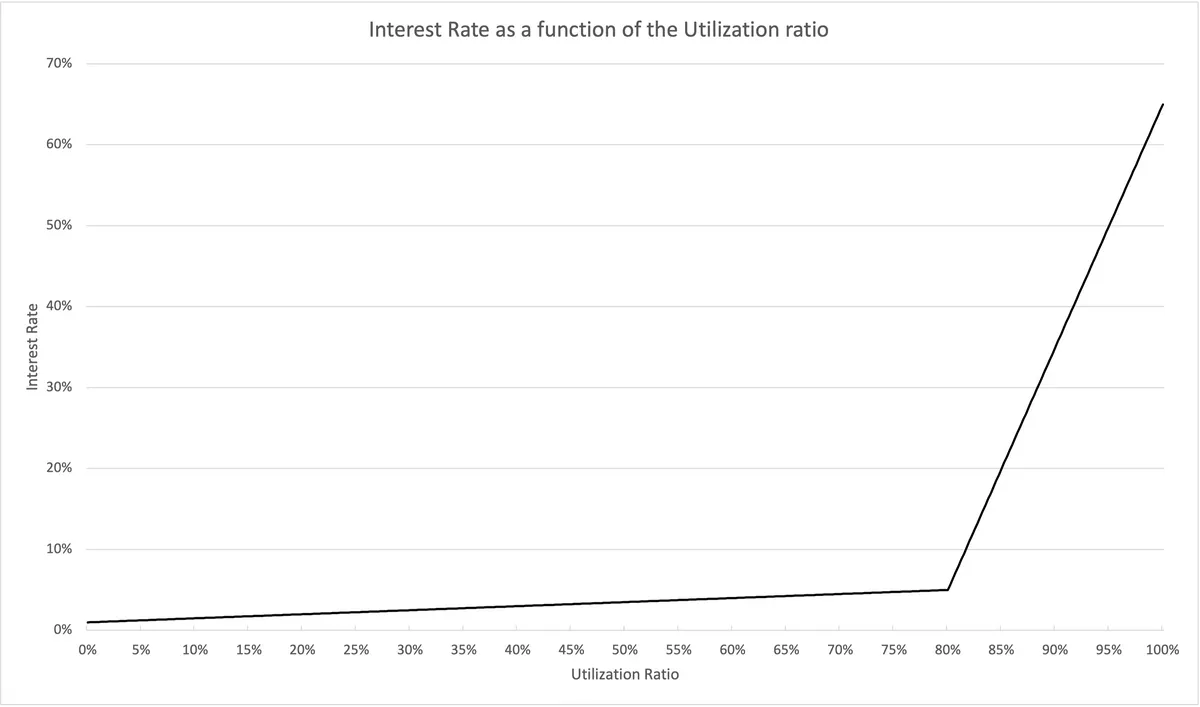

The interest rate depends on the Utilization Rate (UR) of each of the pools (total borrowed / total deposited) and is dynamically adjusted as part of an incentive model: if the UR is bigger than a Optimal Utilization Ratio (U_opt) defined per asset, the interest rate grows at an accelerated slope to incentivize borrowers to repay their loan, therefore reducing the UR.

When either actor makes a deposit in Folks Finance, an fToken (Folks Finance Deposit Token) is minted by the protocol. This fToken represents ownership of the deposit and is used to calculate the accrual on the deposited asset. It is also this token which is used as collateral for a loan.

Figures 1. and 2. show the daily borrow actions since Folks Finance launch, total and by asset respectively. There is a high activity period from April 4th until April 14th probably driven by the protocol's launch at first and maintained due to the downturn market, which would incentivize borrowers to get the asset which lost price if they believed the assets would increase

Methodology

To identify the borrow transactions, a CTE querying the algorand.application_call_transaction with TRY_BASE64_DECODE_STRING(tx_message:txn:apaa[0]::STRING) = 'b' as a constraint and selecting the borrowing app_id’s as be the assets poolAppId.

Next, each of the borrow and collateral amounts are filtered from the algorand.transfers using the tx_group_id of the borrow transactions. This leaves us with two CTE which will be joined by tx_group_id to get a table with a row per borrow action showing the collateral and the loan amount.

To calculate the collateral and borrowed amount in USD, two additional CTEs query the algorand.prices_swap tabe to calculate the average price for each of the borrowing assets. For the collateral asset, since there is no swaps for the fTokens instead the deposit asset is used to price the collateral in USD - i.e. ALGO for fALGO.

Different queries have been the been used to calculate different metrics:

-

Borrow actions query calculates the number of borrow transactions as

count (tx_group_id)and the volume borrowed assum (bor_amount_usd)both daily and cumulative. -

Collateral ratio query calculates the collateral ratio as borrowed amount in USD divided by collateral amount in USD.

Figures 3. and 4. show the daily and cumulative borrowed amount in USD for each of the assets available from Folks Finance.

A similar trend as in borrow actions can be seen: high volume on the first 20 days of the protocol probably linked to the launch and to a downmarket in mid April, followed by an inactive phase with one outlier on May 3rd, where the total borrowed volume was over 80k USD. This was the date after the announcement of the FIFA sponsorship.

USDC and USDT account for almost 1M USD total borrowed amount. ALGO loan is just over 300k USD, while goETH and goBTC have less significative loan volume.

Figure 5. shows the Average Collateral Ratio by collateral - borrow pair at the time of the loan execution. The highest ratio is for fUSDT-USDC, fUSDC-USDT and fgoETH-goBTC (around 0.8) while the lowest is for fgoBTC-ALGO, fUSDC-ALGO and fgoETH-ALGO (around 0.3).

Comparing these to the U_opt, the highest ratio for fUSDT-USDC and fUSDC-USDT can be explained due to the high U_opt of 0.85, while the fgoETH-goBTC would in this case be paying a premium around 3% for this loan since the U_opt is 0.65.

Figures 6. to 9. show the collateral ratio for each loan of USDC, USDT, goBTC and goETH with fALGO as collateral over time. Dots are marked as above or below the average ratio.

Interestingly, USDC and USDT loans above the average seem to convergence to a maximum of 0.8, which is below the U_opt of 0.85 while goBTC and goETH loans above the average converge above their U_opt of 0.6.

More loans above the average than below are given.

Figures 10. to 13. show the collateral ratio for each loan of USDC, USDT, goBTC and goETH with fALGO as collateral by loan amount. Dots are marked as above or below the average ratio.

The maximum loan value

There is a significant amount of loans below 10 USD (some cases going below 1 cent USD) which I can only explain as test loans from users that want to test the waters before commiting to a bigger loan. I wonder why Folks Finance don't implement a minimum loan amount of i.e. 1 USD to avoid spam/dust problems.

Conclusions

-

A total of 1191 borrow actions for 1.4M USD have been borrowed since Folks Finance launch in April 3rd.

-

Most borrowed assets are USDC (0.7M), USDT (0.3M) and ALGO (0.3M)

-

First half of April saw the biggest activity in borrow actions and in volume. After that, the activity in the protocol has decline significantly

-

fUSDT-USDC and fUSDC-USDT loans have the highest collateral ratio (around 0.8) and still below the Optimal Utilization Ratio and fgoETH-goBTC, which means max interest rate of 7,65%.

-

fgoETH-goBTC has the higest collateral ratio (also 0.8) but this time over the Optimal Utilization Ratio, which sets a premium on the interest rate. For a collateral ratio of 0.8, this would mean around 65% interest. The premium paid over the Optimal Utilization Ratio incentivizes the reduction of the collateral ratio to avoid such high rates.

-

More than half the loans have been executed with fALGO as collateral (725k USD). USDC is by far the most demanded loan asset for these loans, with over 500k USD and more than 300 loan actions.

-

For the loans with fALGO as collateral, mode collateral ratios for USDC (0.70) and USDT (0.56) are below the Optimal Utilization Ratio U_opt, 0.85 for both. goBTC and goETH have a higher mode (0.65 / 0.66) than the Optimal (0.60 for both). I interpret this as goBTC and goETH borrowers are okay with higher interests on their loans while USDC and USDT borrowers set their strategies by optimize the borrow amount for lowest interest rates (institutionalized borrowers?).

Analysis done by @KaskCEA powered by Flipside Crypto