Impermanent Loss on USDC Sushiswap pools

Introducing the Impermanent Loss Tracker dashboard: Unlock valuable insights into impermanent loss in USDC pools on SushiSwap Ethereum.

SushiSwap is a decentralized cryptocurrency exchange built on the Ethereum blockchain, known for its automated market maker (AMM) model. It offers users the ability to trade, swap, and provide liquidity to various digital assets. One of the key features of SushiSwap is its unique liquidity provision mechanism, which involves users contributing to liquidity pools.

Liquidity pools on SushiSwap are formed by users who deposit their assets into smart contracts. These pools facilitate the swapping of tokens without the need for traditional order books and rely on the constant liquidity provided by users. By participating in these pools, users can earn trading fees and receive rewards in the form of SUSHI tokens, the native governance token of the platform.

However, when providing liquidity in a SushiSwap pool, users face the risk of impermanent loss. Impermanent loss refers to the temporary loss of value that liquidity providers may experience due to price volatility in the assets they have deposited. This occurs when the relative price of the assets in the pool changes during the time they are held.

The concept of impermanent loss arises from the fact that the value of the liquidity provider's assets is constantly rebalancing in response to market demand. If the price of one asset in the pool significantly increases or decreases compared to the other, the pool's automated algorithm adjusts the asset ratios to maintain the balance. As a result, liquidity providers may end up with fewer total assets compared to simply holding them individually.

It's important to note that impermanent loss is only temporary. If the prices of the pooled assets revert to their original levels, the loss disappears. Additionally, liquidity providers earn trading fees and rewards, which can offset or even surpass the impermanent loss. Nonetheless, it's a risk that users must consider before deciding to provide liquidity in SushiSwap or any other AMM-based platform.

To mitigate impermanent loss, some users employ strategies such as pairing assets with lower volatility, focusing on stablecoin pairs, or utilizing various hedging techniques. It's also worth noting that impermanent loss is more likely to occur in assets with higher price volatility.

In summary, SushiSwap is a decentralized exchange that allows users to trade and provide liquidity using its automated market maker model. While liquidity providers have the opportunity to earn fees and rewards, they also face the risk of impermanent loss due to price volatility in the assets they have deposited. Understanding and managing this risk is crucial for users participating in SushiSwap's liquidity pools.

This dashboard enables users to take a look at deposits into liquidity pools and measure their impermanent loss at a specific point in time (end block number).

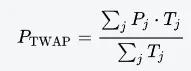

Using swaps data from the selected pool, we’ll take the ratio of USDC and the other token to get the other token’s price in USDC. We’ll average swap prices per block number to get a price sample.

For each deposit, we’ll take note of the price ratio (other token’s price in USDC) at 2 points in time: the time of deposit and the time of the end_block.

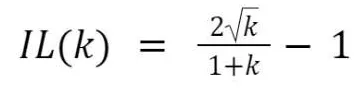

Using the formula on the right, we’ll calculate the impermanent loss (%IL and loss amount) for each deposit.

In order to obtain your desired results, you will have to follow these steps:

- Select a pool address to explore their impermanent loss metrics. You will have to get the pool address on Ethereum.

- Paste the pool address in the pool_address parameter above.

- Click the "Apply All Parameters button".

- Impermanent loss at the time of the end_block is shown.

Please, take into account that the default pool is the WETH/USDC.

The charts you are observing are:

-

Derived time-weighted average token prices (TWAP) using swaps data from a liquidity pool.

-

Calculated impermanent loss over the past year.

-

Characterized impermanent loss with respect to:

- token price

- percent change in relative price

- time of deposit

-

Built an interactive dashboard to compare impermanent loss per deposit for any USDC pool in Ethereum on Sushiswap.

-

Impermanent Loss volatility and average movement

For each block number, we’ll take a time-weighted average price from 100 blocks prior up to corresponding block. The TWAP formula is as follows:

The possibility and magnitude of impermanent loss depend on the price movement of the pooled assets. Here are a few scenarios:

-

Prices remain stable: If the prices of the assets in the pool remain relatively stable, impermanent loss is minimal or non-existent. The liquidity provider can earn trading fees and rewards without experiencing significant fluctuations in the value of their deposited assets.

-

Prices move in the same direction: If the prices of both assets increase or decrease proportionally, impermanent loss is again minimal. The liquidity provider's total value will closely track the price movements of the individual assets.

-

Prices diverge: Impermanent loss becomes more significant when the prices of the pooled assets diverge. If one asset experiences a substantial increase or decrease in price compared to the other, the automated algorithm rebalances the asset ratios to maintain equilibrium. This results in the liquidity provider's assets being skewed towards the underperforming asset, causing a temporary loss in value.

It's important to note that impermanent loss is a risk that liquidity providers face in AMM platforms, but it's not a guaranteed loss. If the prices of the pooled assets revert back to their original levels, the impermanent loss disappears. Furthermore, liquidity providers can still earn trading fees and rewards, which can offset or even surpass the impermanent loss.

In summary, impermanent loss occurs when the value of assets held in a liquidity pool diverges from what it would have been if the assets were held individually. The possibility and magnitude of impermanent loss depend on the price movement of the pooled assets. While impermanent loss is a risk, liquidity providers can potentially mitigate or offset it through trading fees, rewards, and careful selection of asset pairs.

Impermanent loss is closely tied to the relative price change between the assets in a liquidity pool. Let's explore how impermanent loss relates to different scenarios of relative price movements.

-

Stable relative prices: When the relative prices of the assets in the pool remain stable, impermanent loss is minimal. The liquidity provider's assets will maintain their proportional value, and the impact on their total value will be negligible. In this case, providing liquidity can be relatively safe from impermanent loss.

-

Proportional price increase or decrease: If the relative prices of the assets in the pool increase or decrease proportionally, impermanent loss is also minimized. The liquidity provider's assets will increase or decrease in value together, resulting in a balanced outcome. Although impermanent loss may still exist, it will be less significant compared to scenarios with diverging prices.

-

Diverging relative prices: Impermanent loss becomes more pronounced when the relative prices of the pooled assets diverge. If one asset experiences a significant increase or decrease in price compared to the other, impermanent loss occurs as the automated algorithm rebalances the asset ratios.

-

Asset Appreciation: If one asset appreciates significantly relative to the other, the liquidity provider's assets will be skewed towards the underperforming asset due to rebalancing. As a result, the liquidity provider's total value will be lower than if they had held the assets individually during the price increase. Asset Depreciation: Conversely, if one asset depreciates significantly relative to the other, the liquidity provider's assets will be skewed towards the depreciating asset, leading to a temporary loss in total value compared to holding the assets individually. It's important to understand that impermanent loss is not a permanent loss but rather a temporary fluctuation in value. If the relative prices of the pooled assets revert back to their original levels, the impermanent loss diminishes, and the liquidity provider can recover their initial value.

Managing impermanent loss requires careful consideration of the potential price movements of the assets and the risk tolerance of liquidity providers. Strategies such as selecting asset pairs with lower volatility, focusing on stablecoin pairs, or employing hedging techniques can help mitigate the impact of impermanent loss.

In summary, impermanent loss is closely related to the relative price change between the assets in a liquidity pool. When the relative prices remain stable or move proportionally, impermanent loss is minimal. However, when the relative prices diverge significantly, impermanent loss becomes more significant, affecting the liquidity provider's total value temporarily. Implementing appropriate strategies can help liquidity providers manage the impact of impermanent loss.

Impermanent loss is not directly influenced by the duration of time a liquidity provider's assets are deposited in a liquidity pool. Impermanent loss primarily depends on the relative price change between the assets in the pool, rather than the length of time the assets are held.

The concept of impermanent loss is rooted in the constant rebalancing of asset ratios within the liquidity pool based on market demand. This rebalancing happens continuously as trades occur within the pool, and it aims to maintain equilibrium between the assets. The liquidity provider's assets are subject to impermanent loss when the prices of the pooled assets diverge significantly.

The duration of time the assets are deposited only affects the duration of exposure to potential impermanent loss. The longer the assets remain in the pool, the longer the liquidity provider is exposed to the possibility of experiencing impermanent loss. However, the magnitude of impermanent loss is determined by the price movement of the assets during that time period, rather than the duration itself.

It's important to note that impermanent loss is not permanent and can be mitigated or even offset by trading fees and rewards earned by liquidity providers. If the relative prices of the assets revert to their original levels, the impermanent loss disappears, and the liquidity provider's assets return to their initial value.

In summary, impermanent loss is primarily influenced by the relative price change between the assets in a liquidity pool, rather than the duration of time the assets are deposited. The length of time affects the exposure to potential impermanent loss, but the magnitude of impermanent loss is determined by the price movement during that period.

The concept of impermanent loss has garnered significant attention and analysis since the advent of automated market maker (AMM) platforms. Over time, there has been a growing understanding of impermanent loss and its implications for liquidity providers.

While impermanent loss is influenced by various factors such as price volatility, liquidity pool design, and trading volume, it's important to note that the actual magnitude of impermanent loss can vary across different liquidity pools. The specific assets paired in a pool and their respective price movements play a crucial role in determining the extent of impermanent loss experienced by liquidity providers.

In the case of the default pool of WETH/USDC, which pairs Wrapped Ethereum (WETH) with USD Coin (USDC), it's been observed that the impermanent loss has fluctuated between -15% and -30% over the past year. This means that liquidity providers in this particular pool have experienced temporary losses ranging from 15% to 30% of their potential gains if they had held the assets individually during periods of relative price divergence.

Furthermore, the statement mentions that the default pool has had more negative values for impermanent loss over the past months. This suggests that the relative price movements of WETH and USDC have been less favorable for liquidity providers during that time, resulting in higher impermanent loss percentages.

It's worth noting that impermanent loss can be influenced by a range of market conditions, including factors like market sentiment, overall price volatility, and external events impacting the assets in the pool. These factors can contribute to the fluctuations observed in impermanent loss percentages over time.

Liquidity providers should carefully assess the potential risks and rewards associated with providing liquidity in different pools. It's important to consider factors such as the historical performance of the pool, the volatility of the assets, and the individual's risk tolerance when deciding to participate.

In summary, the understanding of impermanent loss has evolved over time, and it remains an inherent risk associated with liquidity provision on AMM platforms. The specific assets paired in a liquidity pool and their price movements significantly influence the magnitude of impermanent loss. The default pool of WETH/USDC has experienced fluctuations between -15% and -30% in impermanent loss percentages over the past year, with a higher prevalence of negative values in recent months. Evaluating the historical performance and considering the risk factors is crucial for liquidity providers seeking to mitigate the impact of impermanent loss.

Impermanent loss (IL) volatility refers to the degree of fluctuation or variability in the magnitude of impermanent loss experienced by liquidity providers over a specific period. It measures the changing levels of impermanent loss and provides insights into the stability or volatility of the liquidity pool's performance.

In the case of the default pool of WETH/USDC, it is stated that the average IL volatility was initially low, starting at around 0 and gradually increasing to over 5 during the first weeks of the past year. This indicates that the impermanent loss experienced by liquidity providers in the pool was relatively stable initially but became more volatile over time.

The average IL of -22% implies that, on average, liquidity providers in the WETH/USDC pool experienced a temporary loss of 22% of their potential gains compared to holding the assets individually during periods of relative price divergence. It's important to note that this is an average value, and individual liquidity providers may have experienced different levels of impermanent loss based on their specific deposit and withdrawal timings.

The statement mentions that the IL average rapidly dropped from -15% to -25% but then remained relatively stable at these levels. This indicates that the magnitude of impermanent loss experienced by liquidity providers in the WETH/USDC pool decreased initially, likely due to more favorable price movements. However, after this initial drop, the average impermanent loss stabilized around -25% over time, suggesting a relatively consistent level of temporary loss experienced by liquidity providers.

The combination of IL volatility increasing prominently over the first weeks of the past year and the average IL stabilizing around -22% indicates that liquidity providers in the WETH/USDC pool faced a relatively volatile environment initially, which then settled into a more stable pattern of impermanent loss.

Analyzing the IL volatility and average IL provides liquidity providers with insights into the historical performance and potential risks associated with participating in a particular liquidity pool. It allows them to evaluate the potential fluctuations in impermanent loss and make informed decisions regarding their liquidity provision strategies.

In summary, IL volatility measures the variability in impermanent loss experienced by liquidity providers in a pool. The default pool of WETH/USDC had an average IL volatility that increased from 0 to over 5 during the first weeks of the past year before stabilizing around 4. The average IL rapidly dropped from -15% to -25% and remained relatively stable at that level. These statistics indicate a relatively volatile environment initially, followed by a more stable pattern of impermanent loss experienced by liquidity providers in the WETH/USDC pool.

- Impermanent loss (IL) is a risk that liquidity providers face when participating in automated market maker (AMM) platforms like SushiSwap.

- IL is primarily influenced by the relative price change between the assets in a liquidity pool.

- The duration of time assets are held in a pool does not directly impact the magnitude of IL but affects the exposure to potential IL.

- The specific assets paired in a liquidity pool and their price movements play a crucial role in determining the extent of IL experienced by liquidity providers.

- The default pool of WETH/USDC in SushiSwap has experienced fluctuating levels of IL, averaging around -22% over time.

- IL volatility measures the variability in the magnitude of IL experienced by liquidity providers.

- The IL volatility of the WETH/USDC pool increased prominently over the first weeks of the past year, settling around 4 thereafter.

- The average IL of the WETH/USDC pool dropped rapidly from -15% to -25% but then remained relatively stable at those levels.

- Historical analysis of IL volatility and average IL provides insights into the stability or volatility of a liquidity pool's performance.

- Liquidity providers should carefully consider the risks and rewards associated with providing liquidity, evaluate historical performance, and employ strategies to mitigate the impact of IL.