FloorDAO: FLOOR Tokens

In the last 90 days, what are users doing with their FLOOR tokens?

Are they staking/unstaking? Swapping for another asset? Are the rebase rewards received from staking FLOOR enough to incentivize users to continue staking? Why or why not?

1. Introduction

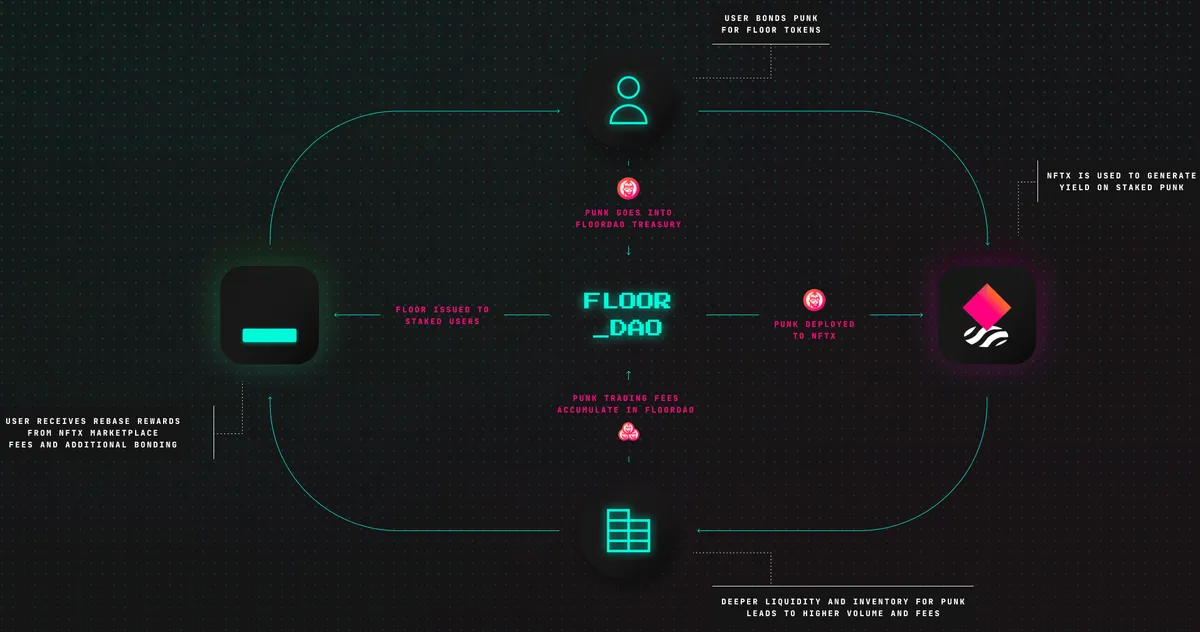

FloorDAO is a decentralized NFT market-making protocol. It enables deep, sticky liquidity for all NFT collections contained in the FloorDAO treasury. FloorDAO uses the bond & rebase mechanisms pioneered by OlympusDAO to accumulate productive NFT liquidity, which is then deployed in strategies such as NFTX vaults to generate yield.

2. Statement of Problem

In this bounty it is requested to investigate how users are utilizing their Floor tokens. To be specific, the following questions will be addressed:

-

Are users staking/unstaking their Floor tokens? The volume of staking/unstaking of Floor tokens were evaluated from “flipside_prod_db.ethereum.udm_events” table where: contract_address = ‘0xf59257e961883636290411c11ec5ae622d19455e’ for Floor tokens and contract_address = ‘0x164afe96912099543bc2c48bb9358a095db8e784’ for sFloor tokens.

-

Are users swapping Floor tokens for another asset? The volume of swaps for/from Floor tokens have been evaluated from “flipside_prod_db.ethereum.dex_swaps” table where: token_address = '0xf59257e961883636290411c11ec5ae622d19455e'.

-

Are the rebase rewards received from staking FLOOR enough to incentivize users to continue staking? Why or why not? Rebase rewards were found from “flipside_prod_db.ethereum.udm_events” where: contract_address = '0xf59257e961883636290411c11ec5ae622d19455e' and ORIGIN_FUNCTION_SIGNATURE = '0xaf14052c' and EVENT_NAME = 'transfer'. It is investigated if there is any relation between staking volume and rebase rewards which users received. Also, the effects of price fluctuation of ETH and Floor tokens are included in the study.

3. Results

3.1. Staking/Unstaking Volume of Floor Tokens

Figure 1 shows the staking/unstaking volume of Floor tokens on a daily basis. The staking and unstaking volumes are both changing in same pattern. At each day the difference between staking and unstaking is negligible but most of the time the staking volume is greater than unstaking volume.

To provide a better view to compare the staking/unstaking volume of Floor tokens, the stake ratio parameter is calculated on a daily basis as follow:

Stake Ratio (%) = 100 * Stake Volume / (Stake Volume + Unstake Volume)

Stake ratio greater than 50% means that at that day the staking volume is greater than unstaking volume. Figure 2 depicts the stake ratio of Floor tokens on a daily basis. Although most of data is below the 50% line, but there are some strong peaks of more than 60%.

Total volume of staking/unstaking of Floor tokens are compared in figure 3. It is revealed that staking volume is 9% larger than unstaking volume.

3.2. Swapping For/From Floor Tokens

The swap volume for/from Floor tokens are given in figure 4. Also in this case, same pattern of increase and decrease are being followed by swap volume for/from Floor tokens. Given the results in figure 4, it is expected that the volume of swaps for/from Floor tokens be nearly close.

Same as staking/unstaking, a swap ratio is calculated as follow:

Swap Ratio (%) = 100 * Swap Volume For Floor / (Swap Volume For Floor + Swap Volume From Floor)

When swap ratio is greater than 50%, it can be concluded that the swap volume for Floor is greater than swap volume from Floor. Figure 5 displays the swap ratio of Floor tokens on a daily basis. It is revealed that most of the data is below the 50% line.

Total volume of swaps for/from Floor tokens is compared in figure 6. As it was expected the swap volume from Floor is 2.6% larger than swap volume for Floor.

3.3. Rebase Rewards Effects on Incentivizing Users to Continue Staking

As mentioned before, when stake ratio is greater than 50%, the Floor stake volume is larger than unstaking volume. On the other hand, one may expect that rebase rewards can incentivize users to continue their staking if it is large enough. As a result, if rebase rewards act as a good motivation for users, there should be a strong relation between stake ratio and rebase rewards.

In figure 7, the stake ratio is plotted against rebase rewards received by users. The findings revealed that there is weak-to-medium correlation between these two parameters. But in general, as rebase rewards increase, the stake ratio also increases.

It cannot be feasible to expect users continue to staking of their Floor tokens just based on rebase rewards. In addition, the crypto market condition must be taken into account. To this end, the average daily ETH price as an indicator of crypto market condition was extracted and plotted against stake ratio in figure 8. The results show that there is no relation between stake ratio and ETH price.

To fill this gap, the absolute daily ETH price fluctuation has been calculated for better representation of crypto market condition and plotted against stake ratio. As demonstrated in figure 9, most of stake ratio greater than 50% is located where ETH price fluctuation is less than 3%. This means that users prefer to continue Floor staking when crypto market is experiencing less volatility.

The same is done and stake ratio has been investigated against daily average price of Floor tokens and its absolute price fluctuation in figures 10 and 11. Also in this case, there is not a strong relation between stake ratio and Floor price. But, most of stake ratio greater than 50% has happened when Floor price fluctuation is less than 20%.

Given the results found in this section, it can be concluded that the willingness of users to continue Floor staking cannot be measured just base on one single parameter. It might be expected that stake ratio is a more complex function of several parameters. To meet this need, stake ratio was examined against the rebase rewards divided by absolute ETH price fluctuation. Findings shown that rebase rewards increase the willingness of users to continue staking and on the other hand, as price fluctuation of ETH decreases the users tends to keep their staking position. Figure 12 shows the stake ratio as a function of rebase rewards divided by ETH price fluctuation. It can be seen that as the reward-to-ETH price fluctuation increases, the stake ratio also increases in a nonlinear manner.

Author believes that this issue requires more in-depth studies. Also, it should be taken into consideration that the number of data availability on Flipside tables is very low, and with such low numbers of data no precise investigation can be conducted.

4. Conclusion

In this bounty, the actions taken by users on their Floor tokens was the subject of the study. Staking/Unstaking Volume, swapping for/from Floor tokens and rebase rewards have been included in this dashboard. The following results can be drawn from this study:

a. Both staking and unstaking volumes of Floor tokens follow same pattern of increase and decrease.

b. The difference between staking and unstaking volumes is relatively small on a daily basis.

c. In total, the staking volume is 9% greater than unstaking volume.

d. The increase and decrease trends in swapping for/from Floor tokens are nearly the same.

e. Swap Ratio for most of the data is less than 50%. But there is some large swap ratio on the data.

f. The swap volume from Floor is just 2.6% greater than swap volume for Floor tokens.

g. No strong relation between stake ratio (willingness of users to continue staking) rebase rewards and price of ETH and Floor tokens can be found.

h. Stake ratio is more related to price fluctuation of ETH and Floor tokens.

i. As the ratio of rewards to ETH price fluctuation increases, the stake ratio also increases in a nonlinear manner.

This study revealed that only rebase reward is not enough to incentivize the users to continue their Floor staking position. Holding a staking position is a complex functions of several parameters such as receiving rewards, crypto market condition (if market is in uptrend or downtrend), discounts offered to stakers and etc. Also, given the low amount of data available, examination of this issue is very challenging.