Terra Seigniorage To Refill Anchor Yield Reserve?

This dashboard aims to analyze what percentage of the seigniorage (LUNA burn) is needed to compensate for the yield deficit on Anchor protocol.

The Health of Anchor Protocol

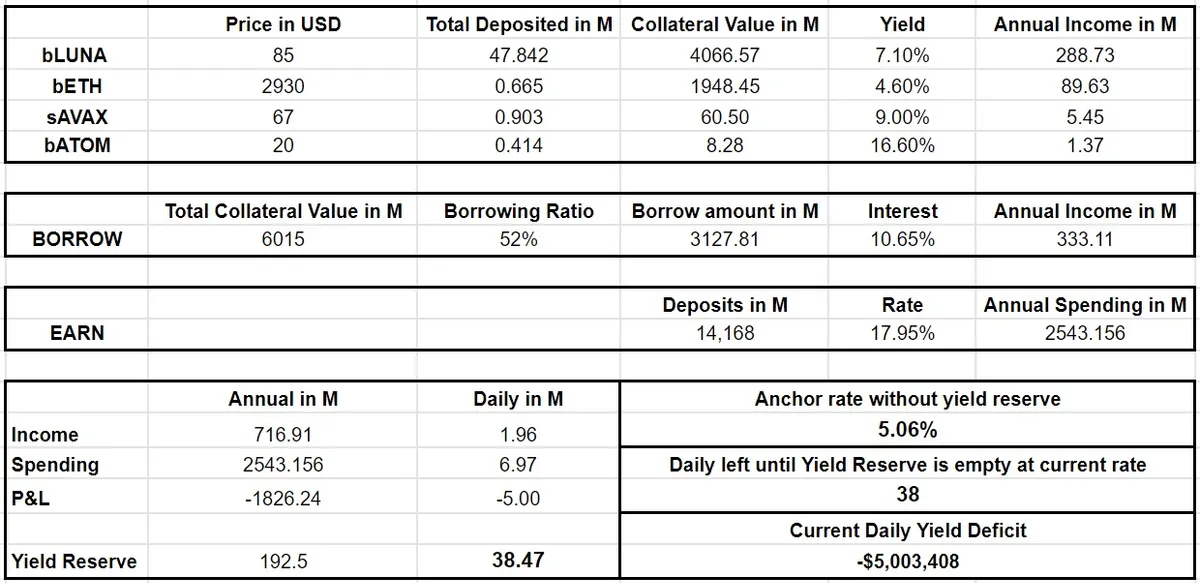

Let's look at the current health of Anchor using the following Sheet. This Sheet uses data from May 5th and can be used to calculate a number of interesting insights about Anchor. For instance, the current Anchor Rate without the Yield Reserve, the remaining amount of days until the Yield Reserve is empty at the current rate, and the daily deficit. We'll be using this Sheet to simulate different scenarios for Anchor.

We can see that at an Anchor Rate of 18%, collateral value of $6B and Earn balance of around $14B, the income deficit is about $5 million per day. This is obviously not sustainable. Therefore, different ideas are proposed to minimize this deficit. Lowering the Anchor Rate by 1.5% per month depending on market conditions has already been implemented. In this dashboard, we'll look at another idea: using a part of the LUNA/UST Seigniorage to refill the Yield Reserve.

Seigniorage is defined as the LUNA that is burned to mint new Terra stablecoins. Before this proposal by Do Kwon, a part of all seigniorage was routed to the community fund and reward LUNA stakers. In the proposal, Do Kwon proposed the permanently burn all seigniorage, which is the current method. In this dashboard, we'll look at the idea of using a part of the seigniorage the compensate for the daily yield deficit on Anchor.

In blue, we can see the total amount of LUNA that is burned per day. In black, the USD value of the burned LUNA is plotted. We can see that the daily amount of LUNA burned ranges anywhere from 1M USD to 180M USD. To deal with this volatility, we'll use different moving averages to estimate the daily amount of USD burned per day. In the chart above, the 30-day moving average is represented using the red line. Currently (May 5th), the 30-day moving average is at about $34M worth of LUNA that is burned per day.

In the chart above, the 3day, 7day, 14day, 20day and 30day moving averages are plotted. Using these moving averages we can better estimate what percentage of the burn is needed to compensate for the current yield deficit of $5M. We can see that on May 5th, the moving averages range from $26M to $56M worth of LUNA that is burned per day.

Knowing the current deficit is about $5M per day, how much of the value of burned LUNA would be needed to compensate for this? Using the different moving averages, we can get an idea of the percentage. On May 5th, the 14-day moving average of the daily USD value of LUNA that was burned was about $56M. Using the chart above, we can see that about 9% of the 14D moving average is needed to compensate for the $5M deficit. The 3D moving average is currently the lowest at $26M. In that case, about 19% of the burned value would be needed to compensate for the deficit. Using these moving averages, we can set a lower and upper bound for the percentage redirect that is needed. From this chart, we can conclude that a redirect between 9% and 19% of the seigniorage would be needed to compensate for the deficit.

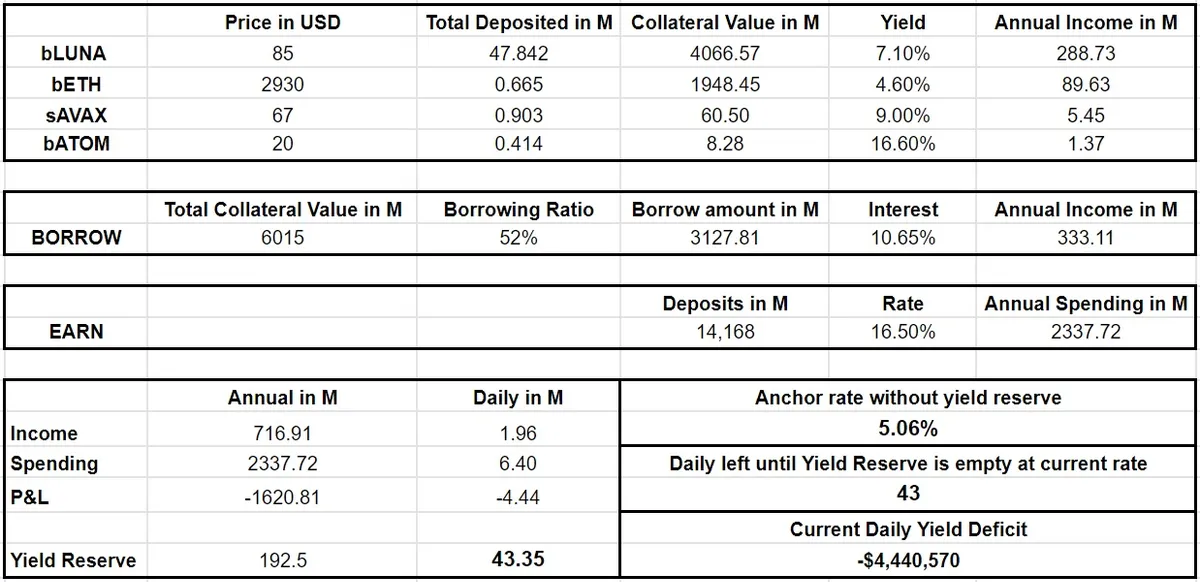

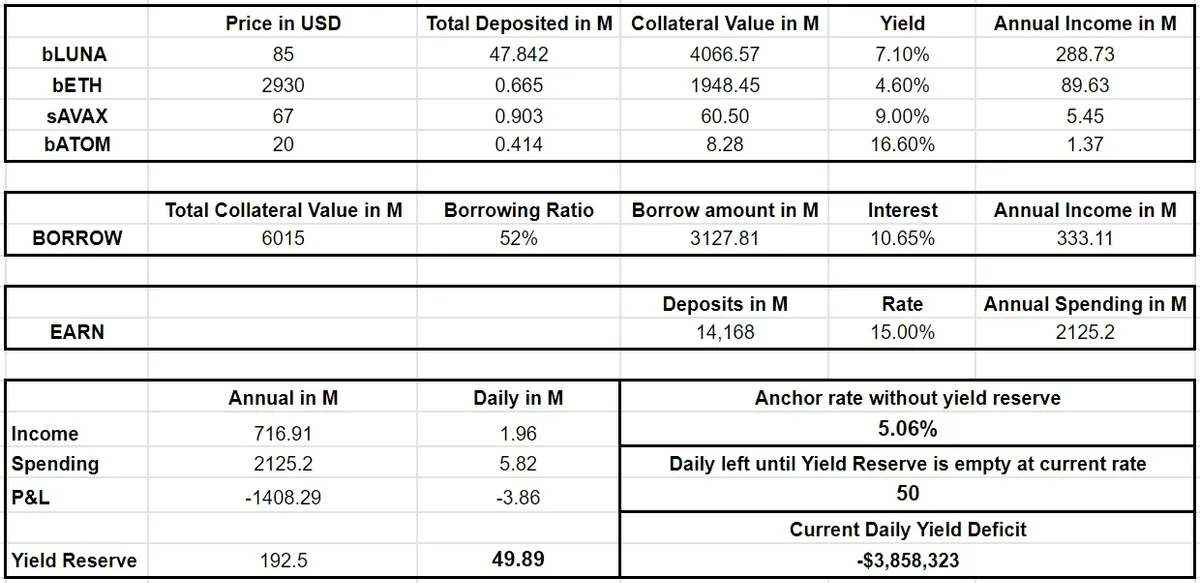

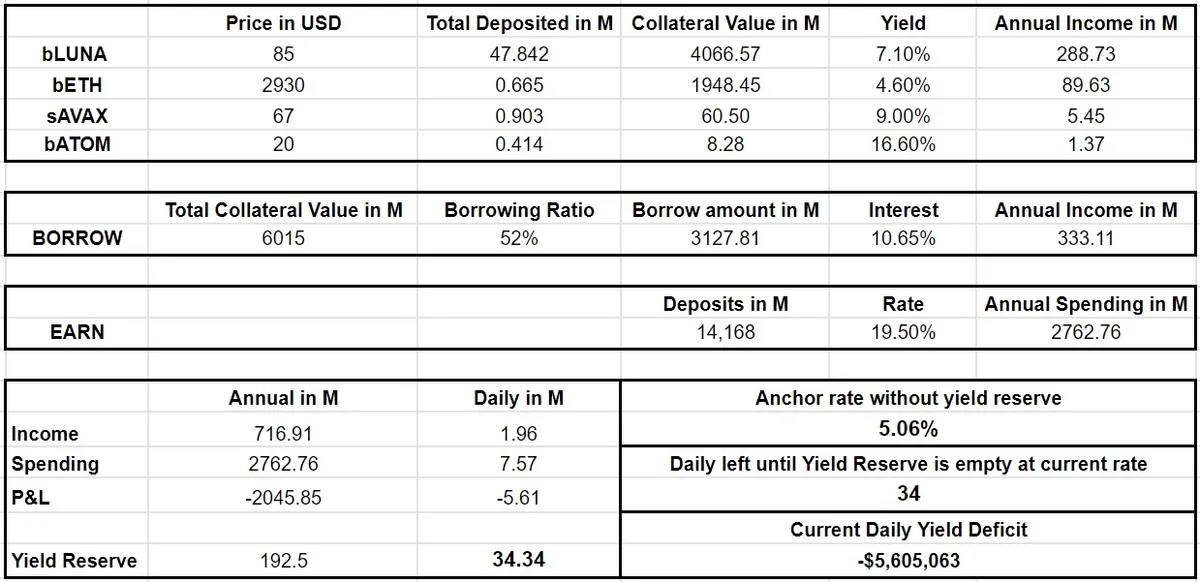

Next, we'll apply the same reasoning for different Anchor Rates. We'll estimate the yield deficit for each Anchor Rate by keeping all other variables the same.

Using the simulating above we get the following yield deficits per Anchor rate:

- 19.5%: $5.6M

- 18%: $5M

- 16.5%: $4.4M

- 15%: $3.8M

If we apply the same method as before, we get the following % redirect ranges for each Anchor Rate:

- Anchor Rate of 19.5%: 10%-22% redirect

- Anchor Rate of 18%: 9%-19% redirect

- Anchor Rate of 16.5%: 8%-17% redirect

- Anchor Rate of 15%: 7%-15% redirect

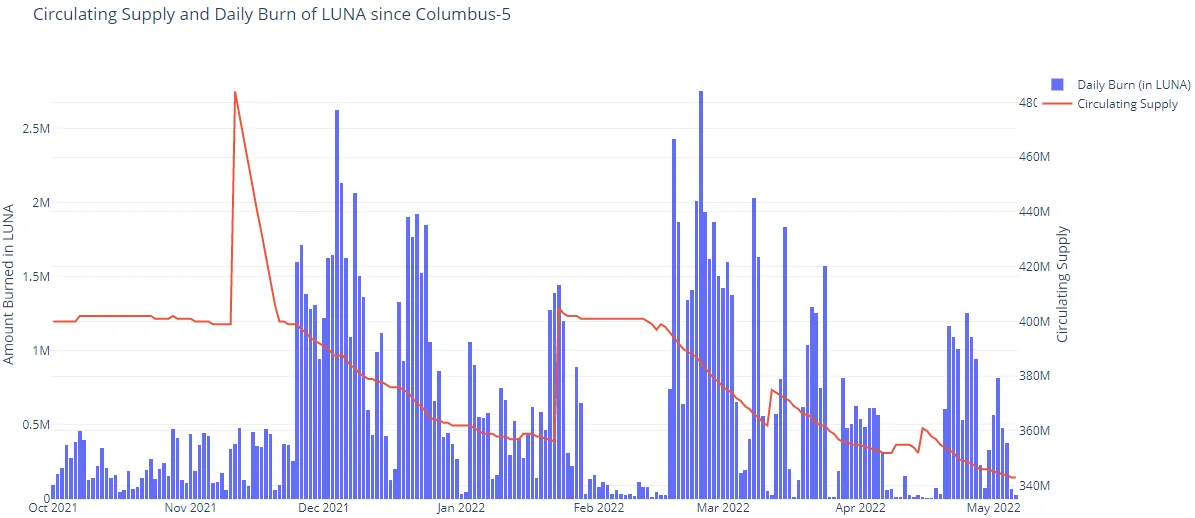

We can clearly see a correlation. In December of 2021, the daily amount LUNA that was burned started to increase, which cause the red line (circulating supply) to go down. We can also see that in February of 2022, when the daily amount of LUNA that was burned was low, the circulating supply was constant as well.